Withholding Tax (WHT) is a tax deducted at source on cross-border income such as dividends, interest, or royalties paid to a UK resident. It represents an advance payment of income tax withheld by the foreign payer before the funds are received.

For UK taxpayers, this income remains taxable under HMRC rules, making the prevention of double taxation essential. Relief is usually available through the UK’s network of Double Taxation Treaties (DTTs) and can be claimed using forms such as HMRC Form DT-Individual or DT-Company.

Understanding withholding tax UK obligations ensures accurate reporting within your Self-Assessment or Corporation Tax return, maximising legitimate treaty reliefs and minimising exposure to unnecessary foreign tax.

What is Withholding Tax?

To truly grasp the impact of WHT on your financial affairs, we must first establish a precise withholding tax meaning.

Withholding Tax (often abbreviated as WHT) is not a separate tax system, but rather a mechanism for collecting income tax. It is a portion of an income payment, such as a dividend, royalty, or interest that the payer is required by law to deduct and remit directly to their local tax authority before the payment is forwarded to the recipient.

A Simple Illustration of How WHT Works

Imagine a UK taxpayer (Recipient) owns shares in a company in Country X (Payer).

- Payment: The Country X company declares a £1,000 dividend.

- Deduction: Country X’s tax law mandates a 15% withholding tax. The company deducts £150 (£1,000 x 15%).

- Remittance: The company sends the £150 WHT to the tax authority in Country X.

- Net Receipt: The UK taxpayer receives the net amount of £850.

- UK Obligation: The UK taxpayer must still declare the gross income (£1,000) on their UK tax return. The £150 withholding tax paid in Country X then forms the basis for claiming Foreign Tax Credit Relief (FTCR) against their UK tax bill.

Understanding what is withholding tax is incomplete without recognising its dual purpose: it acts as a streamlined collection method for foreign governments and serves as a tool to ensure non-residents pay tax on income sourced within their borders.

You can also read our more guides on Personal Tax:

What is a Sole Proprietorship? Things You Should Know

How Much Will I Pay Tax on My Bonus in the UK?

The Domestic and International Context of Withholding Tax

When discussing withholding tax UK, it’s essential to differentiate between domestic UK rules and the foreign WHT that UK taxpayers face on international income.

1. Domestic UK ‘Withholding’ Rules

While the UK doesn’t use the term “withholding tax” for many domestic payments in the same way foreign jurisdictions do, the principle of deduction at source is widely applied:

- PAYE (Pay As You Earn): This is, in effect, a form of domestic WHT on employment income, where the employer deducts Income Tax and National Insurance Contributions (NICs) before paying the employee.

- Income Tax on UK Interest: Banks and building societies used to deduct tax from interest payments, but since the introduction of the Personal Savings Allowance (PSA) in 2016, interest has typically been paid gross. Only in specific circumstances (e.g., some non-resident accounts) is a deduction still made. Get more information on personal savings allowance.

- WHT on UK Royalties and Rents (UK Source): The UK does impose a domestic withholding tax requirement on certain payments of annual interest, patent royalties, and some other payments (e.g., payments made to non-residents for UK-source rental income under the Non-resident Landlord Scheme). This is a statutory obligation under UK tax law, requiring the UK payer to deduct basic rate income tax (currently 20%) at source. See HMRC guidance on royalties paid to non-residents and Non-resident Landlord Scheme.

2. International Withholding Tax for UK Taxpayers

The real challenge for the UK taxpayer lies in dealing with the WHT deducted by foreign governments. This is where you must focus on what is withholding tax in the context of international trade and investment.

| Income Type | Typical Payer Location | Typical WHT Rate (Without DTT) | UK Tax Treatment |

| Dividends | US, Europe, Asia | Up to 30% | Taxable as dividend income in the UK. |

| Interest | Foreign bank/bond issuer | 0% to 35% | Taxable as savings income in the UK. |

| Royalties | Foreign company licensing IP | 10% to 25% | Taxable as trading or miscellaneous income in the UK. |

| Pensions/Annuities | Foreign pension provider | Varies | Taxable as pension income in the UK. |

The headline WHT rates (the ‘Up to 30%’ column) are often the starting point, but they are rarely the final rate that a UK taxpayer must endure, thanks to Double Taxation Treaties.

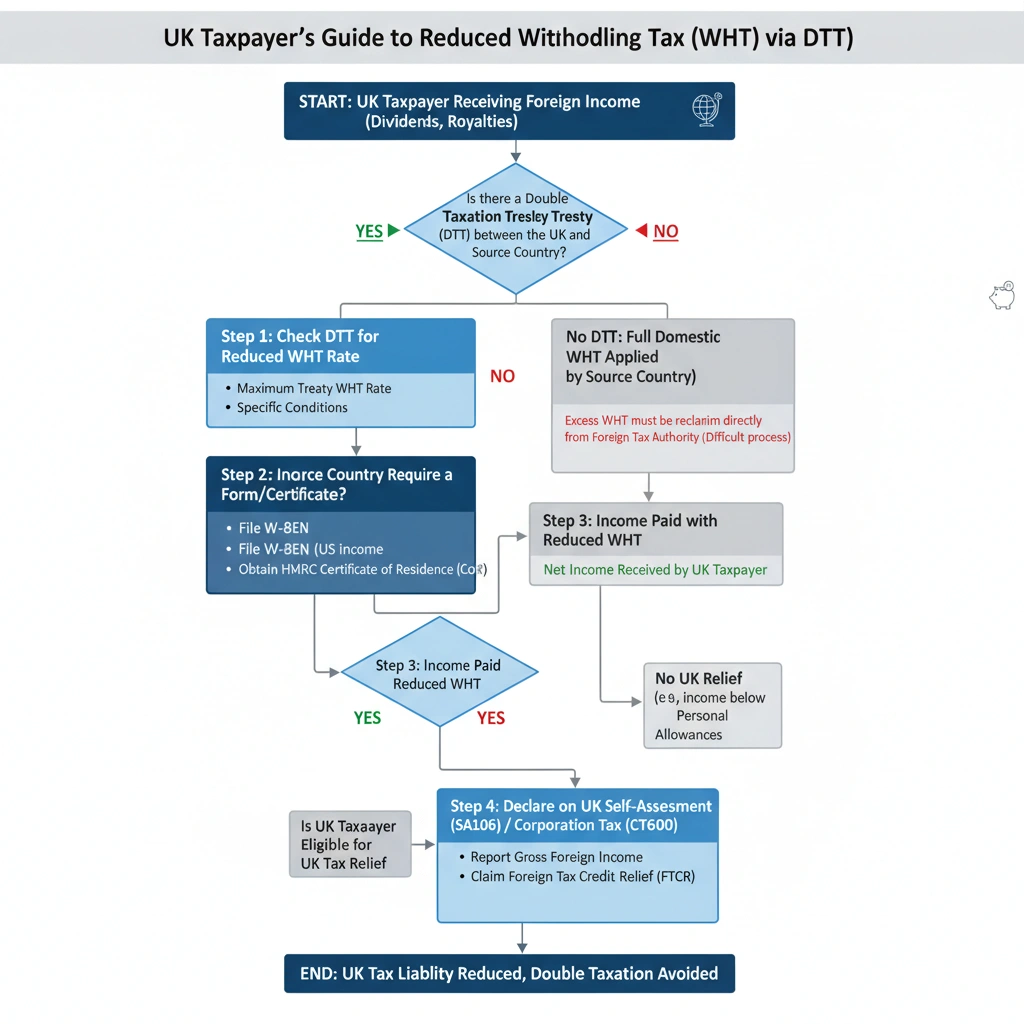

The Critical Role of Double Taxation Treaties (DTTs)

The primary mechanism for mitigating the burden of double taxation where both the source country and the UK taxpayer’s resident country claim the right to tax the same income is the network of Double Taxation Treaties (DTTs) that the UK has negotiated with over 130 countries.

A DTT acts as a binding legal agreement that overrides the domestic tax laws of the treaty partners, specifically setting limits on the amount of WHT that a source country can impose on specific types of passive income paid to a non-resident.

DTTs and Reduced WHT Rates

For a UK taxpayer, a DTT is often the key to achieving a significantly reduced WHT rate. For example:

- US-UK Treaty: The US domestic withholding tax rate on dividends is 30%. However, under the DTT, this rate is typically reduced to 15% for individual investors, or often 0% for UK pension funds or certain corporate structures.

- EU Countries: While EU directives generally aim for low WHT on inter-company payments, for individual UK taxpayers on dividends and interest, DTTs often reduce the standard rate (e.g., 25% or 30%) down to 10% or 15%.

How to Apply for a Reduced Rate

For a UK taxpayer to benefit from the reduced DTT rate, you must prove your status as a UK resident to the foreign payer or tax authority. This process varies by country:

- Self-Certification: The most common method, especially in developed markets, is providing a completed form (such as the US W-8BEN form for US income) to your broker or the paying agent. This certifies you are a foreign beneficial owner and claim treaty benefits, thus ensuring the lower WHT is deducted immediately.

- Certificate of Residence (CoR): For less common jurisdictions or specific types of income, you may need a formal CoR issued by HMRC. This document proves to the foreign tax authority that you are a UK taxpayer and resident, entitling you to the treaty rate.

Expert Note: Failure to file the necessary form (e.g., W-8BEN) will result in the higher domestic WHT being deducted (e.g., 30% in the US). If this happens, you have to reclaim the excess tax from the foreign government, which is a far more arduous and time-consuming process than simply claiming the correct relief in the UK.

Claiming Relief: The UK Taxpayer’s Primary Strategy

The central tenet of international taxation is the obligation of the UK taxpayer to declare their worldwide income. Once you’ve received income net of WHT, your next step is to correctly account for it in the UK and claim relief for the foreign tax paid.

HMRC provides relief primarily through two mechanisms: Foreign Tax Credit Relief (FTCR) and the Deduction Method.

1. Foreign Tax Credit Relief (FTCR)

FTCR is the most advantageous method and the one mandated under most DTTs. It allows the UK taxpayer to offset the foreign WHT paid against the UK tax due on the same income.

The FTCR Golden Rule:

The credit you can claim is the lower of the following two amounts:

- The actual foreign WHT paid (or the amount that would have been payable under the relevant DTT).

- The UK tax liability on that specific foreign income.

| Scenario | Foreign WHT Paid (A) | UK Tax Due (B) | FTCR Allowed (Lower of A or B) |

| WHT is lower than UK tax | £100 | £150 | £100 |

| UK tax is lower than WHT | £100 | £75 | £75 |

What is withholding tax relief? It is the process of eliminating double taxation. If your foreign WHT is higher than your UK tax liability (as in the second scenario above), the excess WHT is lost; it cannot be carried forward, carried back, or offset against UK tax on other income. This is why ensuring the lowest possible WHT rate under the DTT is crucial.

2. The Deduction Method (Less Favourable)

The alternative is the Deduction Method. Under this approach, the foreign WHT is treated as an expense of obtaining the income, meaning it is deducted from the gross foreign income before calculating the UK tax liability.

- Example: Gross Income £1,000, WHT £150.

- FTCR: UK tax is calculated on £1,000, then reduced by a £150 credit.

- Deduction Method: UK tax is calculated on £850 (£1,000 – £150).

The Deduction Method only reduces the taxable income, whereas FTCR reduces the actual tax bill pound-for-pound. For the vast majority of UK taxpayers, FTCR offers superior relief.

Reporting WHT on a UK Tax Return

UK taxpayers must report their foreign income and the WHT deducted via the foreign pages of their Self-Assessment tax return (SA106) or the equivalent box in the Corporation Tax return (CT600).

The correct boxes must be completed with the following figures:

- The gross amount of foreign income.

- The amount of foreign WHT deducted.

- The claim for FTCR.

Pro Tip: When HMRC reviews a Self-Assessment return, they expect the claimed WHT relief not to exceed the treaty rate for the specific country and income type. Claiming a higher rate without justification (e.g., claiming 30% US WHT relief without proving all DTT routes were exhausted) is a common error that triggers HMRC enquiries.

Types of Income Subject to Withholding Tax

To fully appreciate what is withholding tax, we must look at the specific types of income it typically targets internationally.

1. WHT on Dividends

Dividends are arguably the most common source of WHT for the average UK taxpayer with a portfolio of international equities.

- Global Standard: Many countries levy WHT on dividends to secure tax revenue from non-resident shareholders. Rates can range from 0% (e.g., in Singapore or Hong Kong) to 35% or more.

- The UK Exception: Since the abolition of the UK dividend tax credit, the UK does not impose WHT on dividends paid by UK companies to non-resident shareholders (except in very rare circumstances involving certain types of preference shares), aligning with its policy of encouraging foreign investment.

2. WHT on Interest

WHT on interest is complex and highly dependent on the nature of the loan or investment.

- Bank Deposits: Interest from bank savings accounts is often subject to a relatively low or 0% WHT under DTTs, as countries typically want to encourage international capital flows.

- Corporate Bonds/Loans: Interest from corporate bonds or certain types of loans is frequently subject to WHT. The withholding tax UK position, for example, is that the UK generally imposes a 20% deduction on payments of ‘yearly interest’ that have a UK source, unless the recipient is entitled to a treaty exemption or is a UK bank.

3. WHT on Royalties

Royalties payments for the use of intellectual property (IP) like patents, copyrights, trademarks, or trade secrets—are a key target for WHT globally.

- IP Nexus: Because the IP is often used within the source country, that country asserts its right to tax the income generated. WHT rates can be high if a DTT isn’t in place, reflecting the perceived value of the economic activity.

- WHT in Practice: A UK taxpayer receiving royalties from a publisher in Germany for a book may find 10% WHT deducted, as stipulated by the UK-Germany DTT, which is then claimed back as FTCR against the UK taxpayer’s income tax liability on the gross royalty amount.

Advanced WHT Scenarios for the UK Taxpayer

A comprehensive guide on what is withholding tax requires covering scenarios beyond simple portfolio investments.

WHT and UK Corporations

For UK companies (Corporation Taxpayers), managing WHT on foreign receipts and payments is a daily compliance issue.

- Receiving Income: UK companies follow the same FTCR principles as individuals but apply the relief against their Corporation Tax liability (CT600).

- Paying Income: A UK company must be extremely diligent about its domestic withholding tax UK obligations, particularly on interest and royalties paid to overseas recipients. Failure to deduct 20% basic rate tax when required can lead to HMRC penalties and an obligation to pay the outstanding tax themselves. The UK payer must complete the appropriate forms (e.g., form CT61 or the non-resident landlord scheme reporting) and remit the tax to HMRC. They must ensure the foreign recipient has properly claimed a DTT exemption or reduced rate before paying gross or at the reduced rate.

WHT on Foreign Pension Income

As more UK taxpayers have worked abroad, foreign pension income has become a relevant area for WHT.

- DTT Priority: The specific DTT almost always dictates the taxing rights. For most countries, certain lump sums and pension annuities are either taxable only in the country of residence (the UK) or are subject to a maximum low WHT in the source country.

- Special Schemes: Transfers of pensions into Qualified Recognised Overseas Pension Schemes (QROPS) also have specific WHT implications upon withdrawal, which require specialist advice to manage.

WHT and Funds/Unit Trusts

When investing via foreign funds (e.g., an Irish-domiciled or Luxembourg-domiciled fund), the WHT can operate at two levels:

- Fund Level: The fund itself receives income (dividends, interest) from its underlying foreign investments, and WHT is deducted from these payments.

- Investor Level: The UK taxpayer receives a distribution from the fund. The fund is typically responsible for passing through the benefit of the WHT it has suffered, allowing the investor to claim the relief. This requires specific documentation (often a tax voucher or statement) from the fund manager detailing the proportion of foreign tax paid.

Compliance, Reporting, and Penalties

Effective WHT management is an exercise in compliance and record-keeping.

Essential Documentation

The UK taxpayer must maintain rigorous records to support any claim for FTCR. Key documents include:

- Dividend/Interest Vouchers: Statements from brokers, banks, or paying agents showing the gross payment, the amount of WHT deducted, and the net payment.

- Foreign Tax Forms (e.g., W-8BEN): Proof that the required documentation was filed to secure the reduced DTT rate.

- Certificates of Residence (CoR): Where required by the foreign tax authority, the CoR issued by HMRC.

HMRC Scrutiny and Penalties

HMRC uses sophisticated data matching techniques, often cross-referencing information received from foreign tax authorities under international agreements (like the Common Reporting Standard – CRS), to identify anomalies in a UK taxpayer’s return.

- Overclaiming FTCR: The most common error is claiming FTCR based on the full statutory WHT rate (e.g., 30%) when the DTT limits it to a lower rate (e.g., 15%). If HMRC discovers this, the taxpayer is liable to pay the difference plus potential interest and penalties for carelessness.

- Failure to Report Gross Income: Only reporting the net income received is incorrect. HMRC requires the gross income figure and the subsequent FTCR claim. This failure can result in significant penalties for under-declaration of income.

Summary Table for WHT Management

| Step | Action Required for UK Taxpayer | ||

| 1. Prevention | File necessary forms (e.g., W-8BEN) to ensure the lowest treaty-agreed WHT is deducted at source. | ||

| 2. Calculation | Calculate the gross foreign income based on the WHT net amount received and the foreign tax rate. | ||

| 3. Reporting | Declare the gross income and the foreign WHT suffered on the SA106/CT600. | ||

| 4. Relief Claim | Claim FTCR, ensuring the claimed relief does not exceed the lower of UK tax or the DTT-limited WHT rate. |

The Future of WHT: A Digital and Globalised Economy

The definition of what is withholding tax is continuously evolving, particularly with the rise of the digital economy and global shifts in taxation policy.

The OECD and BEPS

The Organisation for Economic Co-operation and Development (OECD) has been leading initiatives, most notably the Base Erosion and Profit Shifting (BEPS) project.

BEPS aims to prevent large multinational enterprises (MNEs) from shifting profits to low-tax jurisdictions.

One key outcome affecting WHT is the increased focus on whether passive payments, especially royalties and interest, are being paid legitimately or simply to avoid tax.

This has led to updated DTTs with anti-abuse clauses, meaning a UK taxpayer needs to demonstrate substance for relief to apply a crucial consideration for corporate structures.

Digital Service Taxes (DSTs)

While not strictly a traditional WHT, the proliferation of Digital Service Taxes (DSTs) in various countries (including the UK’s own DST) represents a parallel effort by governments to tax digital services and revenues generated within their borders, regardless of where the company is headquartered.

The interplay between WHT on royalties and the emerging DST framework is a highly complex area of future tax policy that UK taxpayers with significant digital revenue streams must monitor closely.

What is VAT Withholding Tax?

Though not commonly applied in the UK, VAT Withholding Tax is used in some countries, such as Nigeria and Turkey. It involves withholding part of the VAT due from payments and remitting it directly to tax authorities.

The aim is to prevent VAT evasion and ensure compliance. In the UK, this concept is not widely used, but businesses dealing internationally may encounter this mechanism.

What is Withholding Tax on Interest?

Withholding tax on interest occurs when banks or lenders deduct tax from the interest paid to an account holder before they receive it.

In the UK, most interest from banks is paid gross (without tax deducted), but when paid to non-residents, it may attract withholding tax unless exempted by a DTA.

Always check the residency status and applicable tax treaties to determine if WHT applies.

For guidance, HMRC provides a detailed breakdown on interest taxation.

Implications for Freelancers and Small Businesses

If you’re a freelancer, contractor, or small business owner dealing with international clients, you might find that payments received have withholding tax deducted. This can significantly affect your cash flow and profit margins.

To minimise the impact:

- Review tax treaties before entering international agreements.

- Request tax residency certificates from HMRC.

- Clarify terms in contracts regarding net or gross payments.

Being proactive ensures you’re not overpaying tax and helps avoid complications during tax filing.

Final Thoughts: Know Your Tax Obligations

To summarise the withholding tax meaning, it is a mechanism of tax collection at source on cross-border payments, primarily targeting passive income like dividends, interest, and royalties. Mastery lies in:

- Prevention: Proactively securing the lower treaty rate (e.g., through W-8BEN or CoR) to minimise the initial WHT deduction.

- Correction: Accurately calculating the gross income and claiming the appropriate Foreign Tax Credit Relief (FTCR) in the UK via the Self-Assessment or Corporation Tax process.

Ignoring what is withholding tax or mismanaging the relief process is not merely a compliance issue; it is a financial inefficiency that can permanently erode your investment returns.

As a UK taxpayer, your diligence in applying DTTs and correctly reporting the WHT paid ensures you meet your HMRC obligations while fully exploiting the relief available to you, securing your global financial health.

For further insights and updates, always refer to HMRC’s official pages or consult professional bodies like The Chartered Institute of Taxation and ICAS.

Frequently Asked Questions (FAQs)

To further assist UK taxpayers, here are answers to common queries regarding WHT.

Q: Does the UK have a blanket rule for WHT on dividends received by an individual UK taxpayer?

No. The UK does not deduct WHT on dividends paid by UK companies. However, when a UK taxpayer receives foreign dividends, the WHT deducted is determined entirely by the domestic laws and the relevant Double Taxation Treaty (DTT) of the source country. The UK taxpayer then claims relief for this foreign WHT against their UK tax liability.

Q: What is the single biggest mistake UK taxpayers make regarding WHT?

The most common mistake is failing to apply for the reduced DTT rate in the source country before the payment is made. This results in the full, high domestic rate of WHT being deducted (e.g., 30%), and the excess amount above the treaty rate is often extremely difficult to reclaim directly from the foreign tax authority, resulting in a permanent loss of funds. WHT requires proactivity.

Q: If my foreign bank pays interest gross, do I still need to declare it?

Yes. Whether or not WHT has been deducted, the entire gross amount of income received by a UK taxpayer from anywhere in the world must be declared on the Self-Assessment tax return. Payment of interest gross simply means no WHT was deducted; it doesn’t mean the income is tax-free in the UK.

Q: What is the WHT rate between the UK and Australia on interest?

Under the current UK-Australia Double Taxation Convention, the maximum WHT on interest is generally restricted to 10% of the gross amount of the interest. However, for certain types of interest (e.g., bank interest), the rate is often 0%. You must consult the specific article in the DTT, but this illustrates how a DTT limits the potential maximum withholding tax that can be applied.

Q: Is WHT deducted on all international payments?

No. The scope of what is withholding tax typically covers passive income (dividends, interest, royalties). Payments for goods, services, and certain types of trading income are usually classified as business profits, which are generally only taxable in the source country if the recipient has a ‘Permanent Establishment’ (PE) there, and therefore, they are not typically subject to WHT.

The content provided on TaxCalculatorsUK, including our blog and articles, is for general informational purposes only and does not constitute financial, accounting, or legal advice.

You can also visit HMRC’s official website for more in-depth information about the topic.